Mohammad Ghaderi, Sebastien Plante, Nikolai Roussanov & Sang Byung Seo

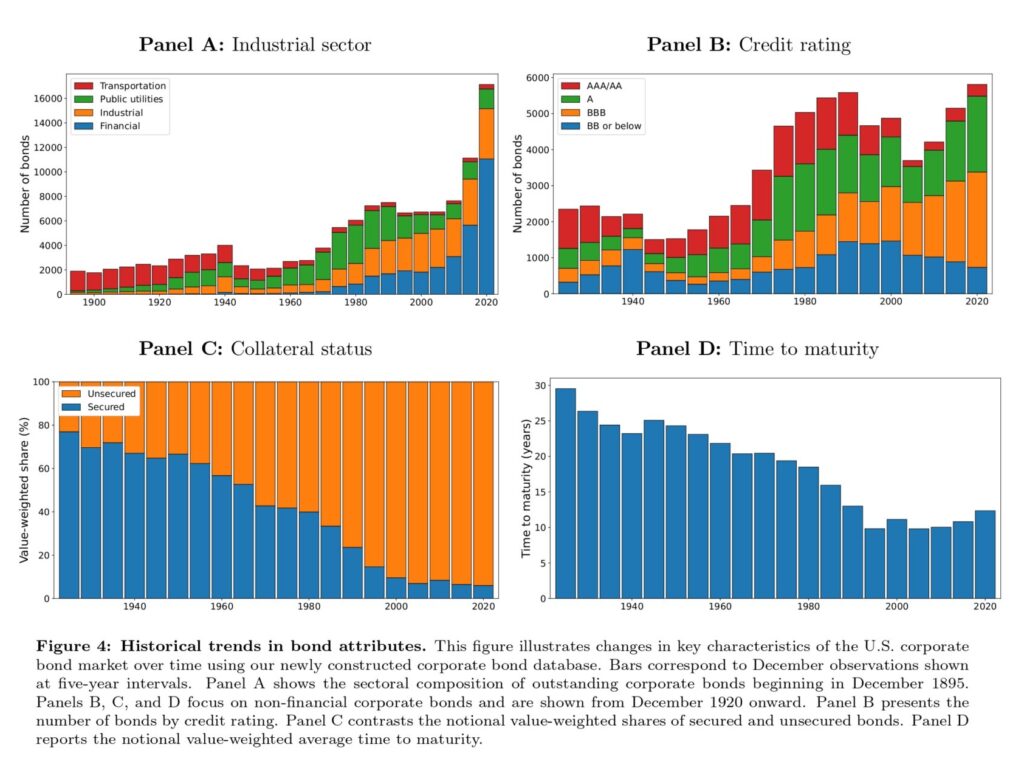

The authors build a new 128-year corporate bond database (1895–2022) — over 100,000 bonds and 7 million observations — by hand-collecting historical bond quotes from archival print sources and merging them with modern data.

Over this long sample, they find a sizable, statistically significant credit risk premium that survives controls for duration and interest rate risk — pushing back on recent work that attributes corporate bond returns mostly to the term premium. Notably, short samples fail to detect this; it only shows up with the century of data.

Credit spreads predict future bond returns and macroeconomic activity, but their power to forecast the business cycle weakens once prewar data and the Great Depression are added — suggesting the spread-economy link is time-varying.

Major equity factors (market, size, value) are also priced in corporate bonds over the long sample, supporting a common factor structure across stocks and bonds rather than segmented markets.

Link to full article: https://papers.ssrn.com/sol3/papers.cfm?abstract_id=6444420