Avaneesh Deleep, John Lee, Jenny Bai, Dhruv Suresh & Harsh Dhawan

Using tick-level order flow, wallet histories, and user commentary across Polymarket and Kalshi, the authors examine who actually generates and exploits pricing inefficiencies in modern prediction markets.

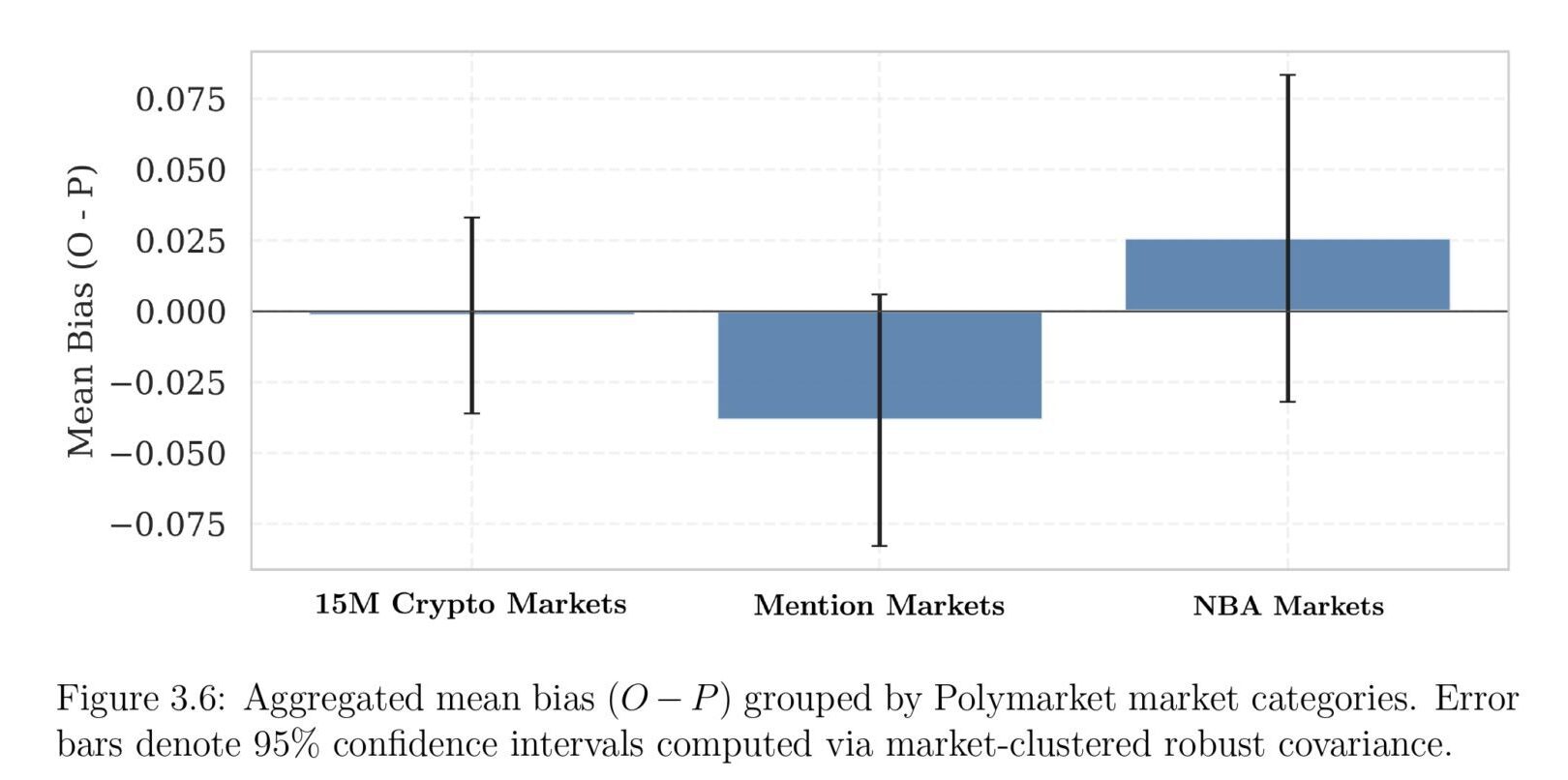

The classic favorite-longshot bias largely disappears once they control for contract lifecycle timing — what looked like that bias in “mention markets” is really a “Yes Bias,” where traders systematically overpay for the affirmative outcome.

“Whales” (the most capitalized traders) aren’t the sharpest; they tend to bleed expected value to small-order traders, trading on ideological conviction and suffering adverse selection.

The loudest participants add no edge — there’s no meaningful correlation between sentiment intensity and informational advantage, so vocal commentary is mostly noise.

Link to full article: https://papers.ssrn.com/sol3/papers.cfm?abstract_id=6322678